1, Types and tools of date and time data

The modules about date, time and calendar data in Python are datatime, time and calendar

**The data types in the datatime module are as follows: from datatime import*****

| data | Use the Gregorian calendar to store calendar dates (year, month, day) |

|---|---|

| time | Store time as hours, minutes, seconds, microseconds |

| datatime | Store date and time |

| timedelta | Represents the difference between two datatime values (such as day, second, microsecond) |

| tzinfo | The basic type used to store time zone information |

datatime formatting details (compatible with ISO C89)

| %Y | Four digit year |

|---|---|

| %y | Two digit year |

| %m | Two digit months [01, 12] |

| %d | Two digit date number [01, 31] |

| %H | Hour, 24-hour system [00, 23] |

| %I | Hour, 12 hour system [01, 12] |

| %M | Two minutes [00, 59] |

| %S | Seconds [00, 61] (60, 61 are leap seconds) |

| %w | Week date [0 (Sunday), 6] |

| %U | Number of weeks in a year [00, 53]. Take Sunday as the first day of the week, and the date before the first week of the year as' week 0 ' |

| %W | Number of weeks in a year [00, 53]. Monday is the first day of the week, and the date before the first Monday of the year is regarded as' week 0 ' |

| %z | UTC time zone offset in the format of + HHMM or - HHMM; Null if there is no time zone |

| %F | %Abbreviation of Y-%m-%d (e.g., 2021-6-24) |

| %D | %Abbreviation for m/%d/%y (e.g., 06 / 24 / 21) |

datatime object locale specific date formatting options

| %a | Abbreviated working day name |

|---|---|

| %A | Full write workday name |

| %b | Abbreviated month name |

| %B | Full month name |

| %c | Full date and time (e.g. 'Tue 01 May 2012 04:20:57 PM') |

| %p | Regional equivalent of AM or PM |

| %x | Format date suitable for the region (for example, '05 / 01 / 2012' in the United States is May 1) |

| %X | Time appropriate for the region (e.g. '04:24:12 PM') |

import numpy as np

import pandas as pd

np.random.seed(12345)

import matplotlib.pyplot as plt

plt.rc('figure', figsize=(10, 6))

PREVIOUS_MAX_ROWS = pd.options.display.max_rows

pd.options.display.max_rows = 20

np.set_printoptions(precision=4, suppress=True)

from datetime import datetime now = datetime.now() now '''datetime.datetime(2021, 6, 24, 16, 47, 28, 879956)''' now.year, now.month, now.day '''(2021, 6, 24)''' # timedelta represents the time difference between two datetime objects delta = datetime(2011, 1, 7) - datetime(2008, 6, 24, 8, 15) delta '''datetime.timedelta(days=926, seconds=56700)''' delta.days '''926''' delta.seconds '''56700''' # Add / subtract a timedelta for the datetime object to generate a new datatime object from datetime import timedelta start = datetime(2011, 1, 7) start + timedelta(12) '''datetime.datetime(2011, 1, 19, 0, 0)''' start - 2 * timedelta(12) '''datetime.datetime(2010, 12, 14, 0, 0)'''

Conversion between string and datatime

# Use the str method or pass a specified format to the strftime method to format the datetime object and the Timestamp object of pandas

stamp = datetime(2011, 1, 3)

str(stamp)

''''2011-01-03 00:00:00''''

stamp.strftime('%Y-%m-%d')

''''2011-01-03''''

# Use datetime Strptime () and format code convert a string to a date

# datetime.strptime() is a good way to convert dates when the format is known

value = '2011-01-03'

datetime.strptime(value, '%Y-%m-%d')

'''datetime.datetime(2011, 1, 3, 0, 0)'''

datestrs = ['7/6/2011', '8/6/2011']

[datetime.strptime(x, '%m/%d/%Y') for x in datestrs]

'''[datetime.datetime(2011, 7, 6, 0, 0), datetime.datetime(2011, 8, 6, 0, 0)]'''

# For the common date format, you can use the parser.xml of the dateutil package Parse method

# dateutil can parse most human understandable date representations

from dateutil.parser import parse

parse('2011-01-03')

'''datetime.datetime(2011, 1, 3, 0, 0)'''

parse('Jan 31, 1997 10:45 PM')

'''datetime.datetime(1997, 1, 31, 22, 45)'''

# Pass dayfirst=True to parse the data whose date is before the month

parse('6/12/2011', dayfirst=True)

'''datetime.datetime(2011, 12, 6, 0, 0)'''

# pd.to_datetime() can convert many different date formats

datestrs = ['2011-07-06 12:00:00', '2011-08-06 00:00:00']

pd.to_datetime(datestrs)

'''DatetimeIndex(['2011-07-06 12:00:00', '2011-08-06 00:00:00'], dtype='datetime64[ns]', freq=None)'''

# pd.to_datetime() can also handle values that are considered missing values (None, empty strings, etc.)

idx = pd.to_datetime(datestrs + [None])

idx

'''DatetimeIndex(['2011-07-06 12:00:00', '2011-08-06 00:00:00', 'NaT'], dtype='datetime64[ns]', freq=None)'''

idx[2] # NaT(Not a time) is a value where the timestamp data value in pandas is null

'''NaT'''

pd.isnull(idx)

'''array([False, False, True])'''

2, Time series basis

The basic time Series type in pandas is Series indexed by timestamp;

pandas is usually represented as a python string or datatime object

from datetime import datetime

dates = [datetime(2011, 1, 2), datetime(2011, 1, 5),

datetime(2011, 1, 7), datetime(2011, 1, 8),

datetime(2011, 1, 10), datetime(2011, 1, 12)]

# Basic time series in pandas: Series indexed by timestamp

ts = pd.Series(np.random.randn(6), index=dates)

ts

'''

2011-01-02 -0.204708

2011-01-05 0.478943

2011-01-07 -0.519439

2011-01-08 -0.555730

2011-01-10 1.965781

2011-01-12 1.393406

dtype: float64

'''

# These datetime objects are actually placed in a DatetimeIndex

ts.index

'''

DatetimeIndex(['2011-01-02', '2011-01-05', '2011-01-07', '2011-01-08',

'2011-01-10', '2011-01-12'],

dtype='datetime64[ns]', freq=None)

'''

# Like other Series, arithmetic operations between time Series with different indexes are automatically aligned by date

ts + ts[::2]

'''

2011-01-02 -0.409415

2011-01-05 NaN

2011-01-07 -1.038877

2011-01-08 NaN

2011-01-10 3.931561

2011-01-12 NaN

dtype: float64

'''

# pandas uses NumPy's datetime64 data type to store timestamps in nanoseconds ns

ts.index.dtype

'''dtype('<M8[ns]')'''

# Each scalar value in DatetimeIndex is the Timestamp object of pandas

stamp = ts.index[0]

stamp

'''Timestamp('2011-01-02 00:00:00')'''

Index, select, subset

# When indexing and selecting based on tags, time series and other pandas Series similar stamp = ts.index[2] ts[stamp] '''-0.5194387150567381''' # Pass a string that can be interpreted as a date, '20110110' is also OK ts['1/10/2011'] '''1.9657805725027142'''

# For long time series, you can pass a string selection data that can be interpreted as a year or year month

longer_ts = pd.Series(np.random.randn(1000),

index=pd.date_range('1/1/2000', periods=1000))

longer_ts

'''

2000-01-01 0.092908

2000-01-02 0.281746

2000-01-03 0.769023

2000-01-04 1.246435

2000-01-05 1.007189

...

2002-09-22 0.930944

2002-09-23 -0.811676

2002-09-24 -1.830156

2002-09-25 -0.138730

2002-09-26 0.334088

Freq: D, Length: 1000, dtype: float64

'''

longer_ts['2001']

'''

2001-01-01 1.599534

2001-01-02 0.474071

2001-01-03 0.151326

2001-01-04 -0.542173

2001-01-05 -0.475496

...

2001-12-27 0.057874

2001-12-28 -0.433739

2001-12-29 0.092698

2001-12-30 -1.397820

2001-12-31 1.457823

Freq: D, Length: 365, dtype: float64

'''

longer_ts['2001-05']

'''

2001-05-01 -0.622547

2001-05-02 0.936289

2001-05-03 0.750018

2001-05-04 -0.056715

2001-05-05 2.300675

...

2001-05-27 0.235477

2001-05-28 0.111835

2001-05-29 -1.251504

2001-05-30 -2.949343

2001-05-31 0.634634

Freq: D, Length: 31, dtype: float64

'''

ts ''' 2011-01-02 -0.204708 2011-01-05 0.478943 2011-01-07 -0.519439 2011-01-08 -0.555730 2011-01-10 1.965781 2011-01-12 1.393406 dtype: float64 ''' # Pass datatime object for slicing ts[datetime(2011, 1, 7):] ''' 2011-01-07 -0.519439 2011-01-08 -0.555730 2011-01-10 1.965781 2011-01-12 1.393406 dtype: float64 ''' # Pass timestamps that are not included in the time series for slicing to perform a range query ts['1/6/2011':'1/11/2011'] ''' 2011-01-07 -0.519439 2011-01-08 -0.555730 2011-01-10 1.965781 dtype: float64 '''

Passing a string that can not be interpreted as a date, a datatime object, or a timestamp for slicing are views that produce the original time series; That is, no data is copied, and the changes on the slice will be reflected on the original data

# The equivalent instance method truncate can slice Series between two dates ts.truncate(before='1/5/2011', after='1/10/2011') ''' 2011-01-05 0.478943 2011-01-07 -0.519439 2011-01-08 -0.555730 2011-01-10 1.965781 dtype: float64 '''

# The above operations also apply to DataFrame

dates = pd.date_range('1/1/2000', periods=100, freq='W-WED')

long_df = pd.DataFrame(np.random.randn(100, 4),

index=dates,

columns=['Colorado', 'Texas',

'New York', 'Ohio'])

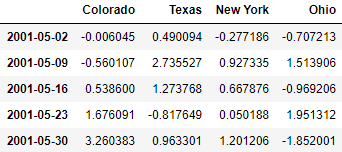

long_df.loc['5-2001']

Time series with duplicate indexes

# There are multiple data observations on a timestamp, that is, the time series contains duplicate indexes

dates = pd.DatetimeIndex(['1/1/2000', '1/2/2000', '1/2/2000',

'1/2/2000', '1/3/2000'])

dup_ts = pd.Series(np.arange(5), index=dates)

dup_ts

'''

2000-01-01 0

2000-01-02 1

2000-01-02 2

2000-01-02 3

2000-01-03 4

dtype: int32

'''

# Through index is_ Unique property to check whether the index is unique

dup_ts.index.is_unique

'''False'''

# When time Series with duplicate indexes are indexed, whether the result is scalar or Series slice depends on whether the timestamp is repeated dup_ts['1/3/2000'] # not duplicated '''4''' dup_ts['1/2/2000'] # duplicated ''' 2000-01-02 1 2000-01-02 2 2000-01-02 3 dtype: int32 '''

# Aggregate data with duplicate indexes and pass level=0 to groupby grouped = dup_ts.groupby(level=0) grouped.mean() ''' 2000-01-01 0 2000-01-02 2 2000-01-03 4 dtype: int32 ''' grouped.count() ''' 2000-01-01 1 2000-01-02 3 2000-01-03 1 dtype: int64 '''

3, Date range, frequency and shift

Generation date range

# pd.date_range(): generate DatatimeIndex of specified length according to specific frequency

# The daily timestamp is generated by default

index = pd.date_range('2012-04-01', '2012-06-01')

index

'''

DatetimeIndex(['2012-04-01', '2012-04-02', '2012-04-03', '2012-04-04',

'2012-04-05', '2012-04-06', '2012-04-07', '2012-04-08',

'2012-04-09', '2012-04-10', '2012-04-11', '2012-04-12',

'2012-04-13', '2012-04-14', '2012-04-15', '2012-04-16',

'2012-04-17', '2012-04-18', '2012-04-19', '2012-04-20',

'2012-04-21', '2012-04-22', '2012-04-23', '2012-04-24',

'2012-04-25', '2012-04-26', '2012-04-27', '2012-04-28',

'2012-04-29', '2012-04-30', '2012-05-01', '2012-05-02',

'2012-05-03', '2012-05-04', '2012-05-05', '2012-05-06',

'2012-05-07', '2012-05-08', '2012-05-09', '2012-05-10',

'2012-05-11', '2012-05-12', '2012-05-13', '2012-05-14',

'2012-05-15', '2012-05-16', '2012-05-17', '2012-05-18',

'2012-05-19', '2012-05-20', '2012-05-21', '2012-05-22',

'2012-05-23', '2012-05-24', '2012-05-25', '2012-05-26',

'2012-05-27', '2012-05-28', '2012-05-29', '2012-05-30',

'2012-05-31', '2012-06-01'],

dtype='datetime64[ns]', freq='D')

'''

# If you pass only a start or end date, you must pass a number for the generation range to periods

pd.date_range(start='2012-04-01', periods=20)

'''

DatetimeIndex(['2012-04-01', '2012-04-02', '2012-04-03', '2012-04-04',

'2012-04-05', '2012-04-06', '2012-04-07', '2012-04-08',

'2012-04-09', '2012-04-10', '2012-04-11', '2012-04-12',

'2012-04-13', '2012-04-14', '2012-04-15', '2012-04-16',

'2012-04-17', '2012-04-18', '2012-04-19', '2012-04-20'],

dtype='datetime64[ns]', freq='D')

'''

pd.date_range(end='2012-06-01', periods=20)

'''

DatetimeIndex(['2012-05-13', '2012-05-14', '2012-05-15', '2012-05-16',

'2012-05-17', '2012-05-18', '2012-05-19', '2012-05-20',

'2012-05-21', '2012-05-22', '2012-05-23', '2012-05-24',

'2012-05-25', '2012-05-26', '2012-05-27', '2012-05-28',

'2012-05-29', '2012-05-30', '2012-05-31', '2012-06-01'],

dtype='datetime64[ns]', freq='D')

'''

# Passing the time series frequency to freq will generate DatatimeIndex falling within the specified date range

pd.date_range('2000-01-01', '2000-12-01', freq='BM')

'''

DatetimeIndex(['2000-01-31', '2000-02-29', '2000-03-31', '2000-04-28',

'2000-05-31', '2000-06-30', '2000-07-31', '2000-08-31',

'2000-09-29', '2000-10-31', '2000-11-30'],

dtype='datetime64[ns]', freq='BM')

'''

# pd.date_range() retains the start or end timestamp by default

# Passing normalize=True normalizes the timestamp to zero, that is, the time in the timestamp is removed

pd.date_range('2012-05-02 12:56:31', periods=5)

'''

DatetimeIndex(['2012-05-02 12:56:31', '2012-05-03 12:56:31',

'2012-05-04 12:56:31', '2012-05-05 12:56:31',

'2012-05-06 12:56:31'],

dtype='datetime64[ns]', freq='D')

'''

pd.date_range('2012-05-02 12:56:31', periods=5, normalize=True)

'''

DatetimeIndex(['2012-05-02', '2012-05-03', '2012-05-04', '2012-05-05',

'2012-05-06'],

dtype='datetime64[ns]', freq='D')

'''

| Base time series frequency | ||

|---|---|---|

| alias | Offset type | describe |

| D | Day | Day of calendar day |

| M | BusinessDay | Every day of the working day |

| H | Hour | Per hour |

| T or min | Minute | per minute |

| S | Second | Per second |

| L or ms | Milli | Per millisecond (1 / 1000 second) |

| U | Micro | Per microsecond (1 / 1000000 second) |

| M | MonthEnd | Last day of the calendar month |

| BM | BusinessMonthEnd | Last day of the month on the working day |

| MS | MonthBegin | First day of the calendar month |

| BMS | BusinessMonthBegin | First day of the month on the working day |

| W-MON,W-TUE,...... | Week | According to the given day of the week, take the day of the week (MON,TUE,WED,THU,FRI,SAT or SUN) |

| WOM-1MON,WOM-2MON,...... | WeekOfMonth | Create week separated dates on the first / second / third or fourth week of the month (e.g. WOM-3FRI: the third Friday of each month) |

| Q-JAN,Q-FEB,...... | QuarterEnd | The quarterly date of the last calendar day of each month to indicate the year in which the month ends (JAN,FEB,MAR,APR,MAY,JUN,JUL,AUG,SEP,OCT,NOV or DEC) |

| BQ-JAN,BQ-FEB,...... | BusinessQuarterEnd | The quarterly date corresponding to the last working day of each month to represent the year when the month ends |

| QS-JAN,QS-FEB,...... | QuarterBegin | The quarterly date corresponding to the first calendar day of each month to indicate the year when the month ends |

| BQS-JAN,BQS-FEB,...... | BusinessQuarterBegin | The quarterly date corresponding to the first working day of each month to represent the year in which the month ends |

| A-JAN,A-FEB,...... | YearEnd | The annual date (JAN,FEB,MAR,APR,MAY,JUN,JUL,AUG,SEP,OCT,NOV or DEC) of the last calendar day of the month in which the given month is located |

| BA-JAN,BA-FEB,...... | BusinessYearEnd | The annual date of the last working day of the month in which the given month is located |

| AS-JAN,AS-FEB,...... | YearBegin | The annual date of the first calendar day of the month in which the given month is located |

| BAS-JAN,BAS-FEB,...... | BusinessYearBegin | The annual date of the first working day of the month in which the given month is located |

Frequency and date offset

# For each base frequency, there is an object that can be used to define the date offset

# For example, the frequency per Hour can be represented by the Hour class

from pandas.tseries.offsets import Hour, Minute

hour = Hour()

hour

'''<Hour>'''

# Pass an integer to define a multiple of the offset

four_hours = Hour(4)

four_hours

'''<4 * Hours>'''

pd.date_range('2000-01-01', '2000-01-03 23:59', freq='4h')

'''

DatetimeIndex(['2000-01-01 00:00:00', '2000-01-01 04:00:00',

'2000-01-01 08:00:00', '2000-01-01 12:00:00',

'2000-01-01 16:00:00', '2000-01-01 20:00:00',

'2000-01-02 00:00:00', '2000-01-02 04:00:00',

'2000-01-02 08:00:00', '2000-01-02 12:00:00',

'2000-01-02 16:00:00', '2000-01-02 20:00:00',

'2000-01-03 00:00:00', '2000-01-03 04:00:00',

'2000-01-03 08:00:00', '2000-01-03 12:00:00',

'2000-01-03 16:00:00', '2000-01-03 20:00:00'],

dtype='datetime64[ns]', freq='4H')

'''

# Multiple offsets can be combined by addition

Hour(2) + Minute(30)

'''<150 * Minutes>'''

pd.date_range('2000-01-01', periods=10, freq='1h30min')

'''

DatetimeIndex(['2000-01-01 00:00:00', '2000-01-01 01:30:00',

'2000-01-01 03:00:00', '2000-01-01 04:30:00',

'2000-01-01 06:00:00', '2000-01-01 07:30:00',

'2000-01-01 09:00:00', '2000-01-01 10:30:00',

'2000-01-01 12:00:00', '2000-01-01 13:30:00'],

dtype='datetime64[ns]', freq='90T')

'''

# Pass freq='WOM-3FRI 'to get the date of the third Friday of a week in the specified date range

rng = pd.date_range('2012-01-01', '2012-09-01', freq='WOM-3FRI')

list(rng)

'''

[Timestamp('2012-01-20 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-02-17 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-03-16 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-04-20 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-05-18 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-06-15 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-07-20 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-08-17 00:00:00', freq='WOM-3FRI')]

'''

Shift date forward or backward

# Shift refers to moving the data in the time series forward or backward in time

# It is implemented through the shift() method of Series or DataFrame

ts = pd.Series(np.random.randn(4),

index=pd.date_range('1/1/2000', periods=4, freq='M'))

ts

'''

2000-01-31 -0.066748

2000-02-29 0.838639

2000-03-31 -0.117388

2000-04-30 -0.517795

Freq: M, dtype: float64

'''

# Shifting data forward introduces a missing value in the start bit

ts.shift(2)

'''

2000-01-31 NaN

2000-02-29 NaN

2000-03-31 -0.066748

2000-04-30 0.838639

Freq: M, dtype: float64

'''

# Shifting data backward will introduce missing values at the end

ts.shift(-2)

'''

2000-01-31 -0.117388

2000-02-29 -0.517795

2000-03-31 NaN

2000-04-30 NaN

Freq: M, dtype: float64

'''

shift() is often used to calculate the percentage change of time series or DataFrame multi column time series, i.e. ts/ts.shift(1)-1

# Passing the frequency freq='M 'to shift will shift the timestamp instead of the data # Here, it means that the timestamp is shifted forward by two months, i.e. + 2 months # Note the difference between the forward shift of data and the forward shift of timestamp ts.shift(2, freq='M') ''' 2000-03-31 -0.066748 2000-04-30 0.838639 2000-05-31 -0.117388 2000-06-30 -0.517795 Freq: M, dtype: float64 ''' # Passing freq='D 'means that each timestamp is shifted forward by 3 days, i.e. + 3 days ts.shift(3, freq='D') ''' 2000-02-03 -0.066748 2000-03-03 0.838639 2000-04-03 -0.117388 2000-05-03 -0.517795 dtype: float64 ''' # # Passing freq='90T 'means that each timestamp is shifted forward by 90 minutes ts.shift(1, freq='90T') ''' 2000-01-31 01:30:00 -0.066748 2000-02-29 01:30:00 0.838639 2000-03-31 01:30:00 -0.117388 2000-04-30 01:30:00 -0.517795 dtype: float64 '''

Shift date using offset

# pandas date offset can also be done using datatime or Timestamp objects

from pandas.tseries.offsets import Day, MonthEnd

now = datetime(2011, 11, 17)

now + 3 * Day()

'''Timestamp('2011-11-20 00:00:00')'''

# Anchor offset, such as MonthEnd, and BusinessMonthEnd will roll forward the date to the next date

now + MonthEnd()

'''Timestamp('2011-11-30 00:00:00')'''

now + MonthEnd(2)

'''Timestamp('2011-12-31 00:00:00')'''

# The anchor offset can be used to scroll the date forward or backward displayed by rollforward and rollback

offset = MonthEnd()

offset.rollforward(now)

'''Timestamp('2011-11-30 00:00:00')'''

offset.rollback(now)

'''Timestamp('2011-12-31 00:00:00')'''

# Use the shift method with groupby

ts = pd.Series(np.random.randn(20),

index=pd.date_range('1/15/2000', periods=20, freq='4d'))

ts

'''

2000-01-15 -0.116696

2000-01-19 2.389645

2000-01-23 -0.932454

2000-01-27 -0.229331

2000-01-31 -1.140330

2000-02-04 0.439920

2000-02-08 -0.823758

2000-02-12 -0.520930

2000-02-16 0.350282

2000-02-20 0.204395

2000-02-24 0.133445

2000-02-28 0.327905

2000-03-03 0.072153

2000-03-07 0.131678

2000-03-11 -1.297459

2000-03-15 0.997747

2000-03-19 0.870955

2000-03-23 -0.991253

2000-03-27 0.151699

2000-03-31 1.266151

Freq: 4D, dtype: float64

'''

# offset.rollforward will operate on the timestamp index of ts by default

ts.groupby(offset.rollforward).mean()

'''

2000-01-31 -0.005833

2000-02-29 0.015894

2000-03-31 0.150209

dtype: float64

'''

# The resample() method can achieve the same effect

ts.resample('M').mean()

'''

2000-01-31 -0.005833

2000-02-29 0.015894

2000-03-31 0.150209

Freq: M, dtype: float64

'''

4, Time zone processing

# The time zone is usually represented as the offset of UTC. The time zone information comes from a third-party library pytz

import pytz

pytz.common_timezones[-5:]

'''['US/Eastern', 'US/Hawaii', 'US/Mountain', 'US/Pacific', 'UTC']'''

# pytz.timezone() gets pytz's time zone object

tz = pytz.timezone('America/New_York')

tz

'''<DstTzInfo 'America/New_York' LMT-1 day, 19:04:00 STD>'''

Localization and conversion of time zones

rng = pd.date_range('3/9/2012 9:30', periods=6, freq='D')

ts = pd.Series(np.random.randn(len(rng)), index=rng)

ts

'''

2012-03-09 09:30:00 -0.202469

2012-03-10 09:30:00 0.050718

2012-03-11 09:30:00 0.639869

2012-03-12 09:30:00 0.597594

2012-03-13 09:30:00 -0.797246

2012-03-14 09:30:00 0.472879

Freq: D, dtype: float64

'''

# Used to return the time zone

print(ts.index.tz)

'''None'''

# Date ranges can be generated from time zone collections

pd.date_range('3/9/2012 9:30', periods=10, freq='D', tz='UTC')

'''

DatetimeIndex(['2012-03-09 09:30:00+00:00', '2012-03-10 09:30:00+00:00',

'2012-03-11 09:30:00+00:00', '2012-03-12 09:30:00+00:00',

'2012-03-13 09:30:00+00:00', '2012-03-14 09:30:00+00:00',

'2012-03-15 09:30:00+00:00', '2012-03-16 09:30:00+00:00',

'2012-03-17 09:30:00+00:00', '2012-03-18 09:30:00+00:00'],

dtype='datetime64[ns, UTC]', freq='D')

'''

ts

'''

2012-03-09 09:30:00 -0.202469

2012-03-10 09:30:00 0.050718

2012-03-11 09:30:00 0.639869

2012-03-12 09:30:00 0.597594

2012-03-13 09:30:00 -0.797246

2012-03-14 09:30:00 0.472879

Freq: D, dtype: float64

'''

# With tz_localize() converts a simple time zone to a localized time zone

ts_utc = ts.tz_localize('UTC')

ts_utc

'''

2012-03-09 09:30:00+00:00 -0.202469

2012-03-10 09:30:00+00:00 0.050718

2012-03-11 09:30:00+00:00 0.639869

2012-03-12 09:30:00+00:00 0.597594

2012-03-13 09:30:00+00:00 -0.797246

2012-03-14 09:30:00+00:00 0.472879

Freq: D, dtype: float64

'''

ts_utc.index

'''

DatetimeIndex(['2012-03-09 09:30:00+00:00', '2012-03-10 09:30:00+00:00',

'2012-03-11 09:30:00+00:00', '2012-03-12 09:30:00+00:00',

'2012-03-13 09:30:00+00:00', '2012-03-14 09:30:00+00:00'],

dtype='datetime64[ns, UTC]', freq='D')

'''

# Localized time zones are available through tz_convert() to another time zone

ts_utc.tz_convert('America/New_York')

'''

2012-03-09 04:30:00-05:00 -0.202469

2012-03-10 04:30:00-05:00 0.050718

2012-03-11 05:30:00-04:00 0.639869

2012-03-12 05:30:00-04:00 0.597594

2012-03-13 05:30:00-04:00 -0.797246

2012-03-14 05:30:00-04:00 0.472879

Freq: D, dtype: float64

'''

# With tz_localize() localizes the time zone to the New York time zone

ts_eastern = ts.tz_localize('America/New_York')

ts_eastern.tz_convert('UTC')

'''

2012-03-09 14:30:00+00:00 -0.202469

2012-03-10 14:30:00+00:00 0.050718

2012-03-11 13:30:00+00:00 0.639869

2012-03-12 13:30:00+00:00 0.597594

2012-03-13 13:30:00+00:00 -0.797246

2012-03-14 13:30:00+00:00 0.472879

dtype: float64

'''

ts_eastern.tz_convert('Europe/Berlin')

'''

2012-03-09 15:30:00+01:00 -0.202469

2012-03-10 15:30:00+01:00 0.050718

2012-03-11 14:30:00+01:00 0.639869

2012-03-12 14:30:00+01:00 0.597594

2012-03-13 14:30:00+01:00 -0.797246

2012-03-14 14:30:00+01:00 0.472879

dtype: float64

'''

# tz_localize(),tz_convert() is also an instance method of DatetimeIndex

ts.index.tz_localize('Asia/Shanghai')

'''

DatetimeIndex(['2012-03-09 09:30:00+08:00', '2012-03-10 09:30:00+08:00',

'2012-03-11 09:30:00+08:00', '2012-03-12 09:30:00+08:00',

'2012-03-13 09:30:00+08:00', '2012-03-14 09:30:00+08:00'],

dtype='datetime64[ns, Asia/Shanghai]', freq=None)

'''

Operation of time zone aware timestamp object

# Separate Timestamp objects can also be localized to time zone aware timestamps and time zone conversion

stamp = pd.Timestamp('2011-03-12 04:00')

stamp_utc = stamp.tz_localize('utc')

stamp_utc.tz_convert('America/New_York')

'''Timestamp('2011-03-11 23:00:00-0500', tz='America/New_York')'''

# Pass time zone when creating Timestamp object

stamp_moscow = pd.Timestamp('2011-03-12 04:00', tz='Europe/Moscow')

stamp_moscow

'''Timestamp('2011-03-12 04:00:00+0300', tz='Europe/Moscow')'''

# The time zone aware Timestamp object stores UTC Timestamp values in nanoseconds since the Unix era (1970-1-1)

stamp_utc.value

'''1299902400000000000'''

# The number of nanoseconds UTC timestamp value is unchanged in time zone conversion

stamp_utc.tz_convert('America/New_York').value

'''1299902400000000000'''

from pandas.tseries.offsets import Hour

stamp = pd.Timestamp('2012-03-12 01:30', tz='US/Eastern')

stamp

'''Timestamp('2012-03-12 01:30:00-0400', tz='US/Eastern')'''

# Hour() added is 1 hour of UTC

stamp + Hour()

'''Timestamp('2012-03-12 02:30:00-0400', tz='US/Eastern')'''

stamp = pd.Timestamp('2012-11-04 00:30', tz='US/Eastern')

stamp

'''Timestamp('2012-11-04 00:30:00-0400', tz='US/Eastern')'''

stamp + 2 * Hour()

'''Timestamp('2012-11-04 01:30:00-0500', tz='US/Eastern')'''

Operation in different time intervals

# Operations in different time intervals will be automatically converted to UTC time first, and the result is also UTC time

rng = pd.date_range('3/7/2012 9:30', periods=10, freq='B')

ts = pd.Series(np.random.randn(len(rng)), index=rng)

ts

'''

2012-03-07 09:30:00 0.522356

2012-03-08 09:30:00 -0.546348

2012-03-09 09:30:00 -0.733537

2012-03-12 09:30:00 1.302736

2012-03-13 09:30:00 0.022199

2012-03-14 09:30:00 0.364287

2012-03-15 09:30:00 -0.922839

2012-03-16 09:30:00 0.312656

2012-03-19 09:30:00 -1.128497

2012-03-20 09:30:00 -0.333488

Freq: B, dtype: float64

'''

ts1 = ts[:7].tz_localize('Europe/London')

ts2 = ts1[2:].tz_convert('Europe/Moscow')

result = ts1 + ts2

result.index

'''

DatetimeIndex(['2012-03-07 09:30:00+00:00', '2012-03-08 09:30:00+00:00',

'2012-03-09 09:30:00+00:00', '2012-03-12 09:30:00+00:00',

'2012-03-13 09:30:00+00:00', '2012-03-14 09:30:00+00:00',

'2012-03-15 09:30:00+00:00'],

dtype='datetime64[ns, UTC]', freq=None)

'''

5, Time interval and interval arithmetic

The Period class represents a time interval, that is, a time range. For example, some days, some months, some quarters, some years

# The following Period objects represent the Period from January 1, 2007 to December 31, 2007

p = pd.Period(2007, freq='A-DEC')

p

'''Period('2007', 'A-DEC')'''

# When doing addition and subtraction, shift directly according to the frequency freq='A-DEC '

p + 5

'''Period('2012', 'A-DEC')'''

p - 2

'''Period('2005', 'A-DEC')'''

# The difference between two intervals with the same frequency is a multiple of the frequency

pd.Period('2014', freq='A-DEC') - p

'''<7 * YearEnds: month=12>'''

# Use PD period_ Range() can construct regular interval sequences

rng = pd.period_range('2000-01-01', '2000-06-30', freq='M')

rng

'''PeriodIndex(['2000-01', '2000-02', '2000-03', '2000-04', '2000-05', '2000-06'], dtype='period[M]', freq='M')'''

# PeriodIndex class stores interval sequence, which can be used as axis index of pandas data structure

pd.Series(np.random.randn(6), index=rng)

'''

2000-01 -0.514551

2000-02 -0.559782

2000-03 -0.783408

2000-04 -1.797685

2000-05 -0.172670

2000-06 0.680215

Freq: M, dtype: float64

'''

# pd.PeriodIndex() generates the PeriodIndex class values = ['2001Q3', '2002Q2', '2003Q1'] index = pd.PeriodIndex(values, freq='Q-DEC') index '''PeriodIndex(['2001Q3', '2002Q2', '2003Q1'], dtype='period[Q-DEC]', freq='Q-DEC')'''

Interval frequency conversion

# Create a Period interval with December as the end month of the year

p = pd.Period('2007', freq='A-DEC')

p

'''Period('2007', 'A-DEC')'''

# asfreq() can convert interval and PeriodIndex objects to other frequencies

p.asfreq('M', how='start')

'''Period('2007-01', 'M')'''

p.asfreq('M', how='end')

'''Period('2007-12', 'M')'''

# Create a Period interval with June as the end month of the year

# In this case, the period from July 2006 to June 2007 is regarded as the year of 2007

p = pd.Period('2007', freq='A-JUN')

p

'''Period('2007', 'A-JUN')'''

# Specifying how as' start 'will return the first month of 2007

# Since June is the end month of the year, the first month is 2006-07

p.asfreq('M', 'start')

'''Period('2006-07', 'M')'''

p.asfreq('M', 'end')

'''Period('2007-06', 'M')'''

# The above is the conversion from low frequency to high frequency, or from high frequency to low frequency, that is, similar month to year

p = pd.Period('Aug-2007', 'M')

p.asfreq('A-JUN')

# When 'A-JUN' is imported, the end month of the table name year is June, so 2007-8 belongs to 2008

'''Period('2008', 'A-JUN')'''

p = pd.Period('Aug-2007', 'M')

p.asfreq('A-SEP')

# When 'A-SEP' is imported, the end month of the table name year is June, so 2007-8 belongs to 2007

'''Period('2007', 'A-SEP')'''

# The complete PeriodIndex object or time series can do the above similar conversion

rng = pd.period_range('2006', '2009', freq='A-DEC')

ts = pd.Series(np.random.randn(len(rng)), index=rng)

ts

'''

2006 1.607578

2007 0.200381

2008 -0.834068

2009 -0.302988

Freq: A-DEC, dtype: float64

'''

ts.asfreq('M', how='start')

'''

2006-01 1.607578

2007-01 0.200381

2008-01 -0.834068

2009-01 -0.302988

Freq: M, dtype: float64

'''

ts.asfreq('B', how='end')

'''

2006-12-29 1.607578

2007-12-31 0.200381

2008-12-31 -0.834068

2009-12-31 -0.302988

Freq: B, dtype: float64

'''

Quarterly interval frequency

# Quarterly data are generally at the end of the fiscal year, so similar to 2012Q4 generally have different meanings

# Set freq='Q-JAN ', indicating that the month at the end of the quarter is January

# Therefore, 2012Q4 refers to the four months from November 2011 to January 2012

p = pd.Period('2012Q4', freq='Q-JAN')

p

'''Period('2012Q4', 'Q-JAN')'''

p.asfreq('D', 'start')

'''Period('2011-11-01', 'D')'''

p.asfreq('D', 'end')

'''Period('2012-01-31', 'D')'''

# Get the timestamp of 4:00 p.m. on the penultimate business day of the quarter

# p. Asfreq ('b ',' e ') - 1 get the penultimate work of the quarter

# (p.asfreq('B', 'e') - 1). Asfreq ('t ','s') converts the obtained date into minutes and is the zero point of the day

# Another '+ 16 * 60' is the number of minutes plus 4 p.m

p4pm = (p.asfreq('B', 'e') - 1).asfreq('T', 's') + 16 * 60

p4pm

'''Period('2012-01-30 16:00', 'T')'''

# Use to_timestamp() to timestamp

p4pm.to_timestamp()

'''Timestamp('2012-01-30 16:00:00')'''

# pd.period_range() is used to generate quarterly series

rng = pd.period_range('2011Q3', '2012Q4', freq='Q-JAN')

ts = pd.Series(np.arange(len(rng)), index=rng)

ts

'''

2011Q3 0

2011Q4 1

2012Q1 2

2012Q2 3

2012Q3 4

2012Q4 5

Freq: Q-JAN, dtype: int32

'''

# Get the timestamp of 4:00 p.m. on the penultimate business day of the quarter

new_rng = (rng.asfreq('B', 'e') - 1).asfreq('T', 's') + 16 * 60

ts.index = new_rng.to_timestamp()

ts

'''

2010-10-28 16:00:00 0

2011-01-28 16:00:00 1

2011-04-28 16:00:00 2

2011-07-28 16:00:00 3

2011-10-28 16:00:00 4

2012-01-30 16:00:00 5

dtype: int32

'''

Convert timestamp to interval (and inverse conversion)

rng = pd.date_range('2000-01-01', periods=3, freq='M')

ts = pd.Series(np.random.randn(3), index=rng)

ts

'''

2000-01-31 1.663261

2000-02-29 -0.996206

2000-03-31 1.521760

Freq: M, dtype: float64

'''

# Series and DataFrame indexed by timestamp are available to_ The period() method is converted to an interval

pts = ts.to_period()

pts

'''

2000-01 1.663261

2000-02 -0.996206

2000-03 1.521760

Freq: M, dtype: float64

'''

rng = pd.date_range('1/29/2000', periods=6, freq='D')

ts2 = pd.Series(np.random.randn(6), index=rng)

ts2

'''

2000-01-29 0.244175

2000-01-30 0.423331

2000-01-31 -0.654040

2000-02-01 2.089154

2000-02-02 -0.060220

2000-02-03 -0.167933

Freq: D, dtype: float64

'''

# After interval conversion, it is allowed that the index contains repeated intervals

ts2.to_period('M')

'''

2000-01 0.244175

2000-01 0.423331

2000-01 -0.654040

2000-02 2.089154

2000-02 -0.060220

2000-02 -0.167933

Freq: M, dtype: float64

'''

# Create JAN-1 as the month at the end of the last quarter of each year

rng = pd.period_range('2011Q3', '2012Q4', freq='Q-JAN')

ts3 = pd.Series(np.arange(len(rng)), index=rng)

ts3

'''

2011Q3 0

2011Q4 1

2012Q1 2

2012Q2 3

2012Q3 4

2012Q4 5

Freq: Q-JAN, dtype: int32

'''

# to_timestamp() converts the interval to a timestamp

# how defaults to start, and takes the zero point of the first month of the quarter as the index; how='end 'can also be set

ts3.to_timestamp()

'''

2010-08-01 0

2010-11-01 1

2011-02-01 2

2011-05-01 3

2011-08-01 4

2011-11-01 5

Freq: QS-NOV, dtype: int32

'''

Generate PeriodIndex from array

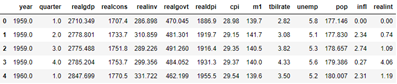

data = pd.read_csv('examples/macrodata.csv')

data.head(5)

data.year.head()

'''

0 1959.0

1 1959.0

2 1959.0

3 1959.0

4 1960.0

Name: year, dtype: float64

'''

data.quarter.head()

'''

0 1.0

1 2.0

2 3.0

3 4.0

4 1.0

Name: quarter, dtype: float64

'''

index = pd.PeriodIndex(year=data.year, quarter=data.quarter,

freq='Q-DEC')

index

'''

PeriodIndex(['1959Q1', '1959Q2', '1959Q3', '1959Q4', '1960Q1', '1960Q2',

'1960Q3', '1960Q4', '1961Q1', '1961Q2',

...

'2007Q2', '2007Q3', '2007Q4', '2008Q1', '2008Q2', '2008Q3',

'2008Q4', '2009Q1', '2009Q2', '2009Q3'],

dtype='period[Q-DEC]', length=203, freq='Q-DEC')

'''

data.index = index

data.head()

6, Resampling and frequency conversion

Resampling: the process of converting a time series from one frequency to another

Down sampling: aggregates higher frequencies to lower frequencies

Up sampling: converts low frequencies to high frequencies

However, not all resampling are the above two types, such as converting W-WED to W-REI

The resample() method of the pandas object performs frequency conversion, which has a function similar to group by

rng = pd.date_range('2000-01-01', periods=100, freq='D')

ts = pd.Series(np.random.randn(len(rng)), index=rng)

ts

'''

2000-01-01 0.631634

2000-01-02 -1.594313

2000-01-03 -1.519937

2000-01-04 1.108752

2000-01-05 1.255853

...

2000-04-05 -0.423776

2000-04-06 0.789740

2000-04-07 0.937568

2000-04-08 -2.253294

2000-04-09 -1.772919

Freq: D, Length: 100, dtype: float64

'''

ts.resample('M').mean()

'''

2000-01-31 -0.165893

2000-02-29 0.078606

2000-03-31 0.223811

2000-04-30 -0.063643

Freq: M, dtype: float64

'''

# kind='period 'specifies that the type of index in the result is period

ts.resample('M', kind='period').mean()

'''

2000-01 -0.165893

2000-02 0.078606

2000-03 0.223811

2000-04 -0.063643

Freq: M, dtype: float64

'''

| Parameters of the resample() method | |

|---|---|

| freq | Sampling frequency, which is a string or DataOffset object (such as' 5min ','M', or Second(1)) |

| axis | Which axis to sample along, the default axis=0 |

| fill_method | The difference method when sampling upward. Interpolation is not allowed by default. Options include 'fill' and 'bfill' |

| closed | In down sampling, which segment of each interval is closed can be 'right' or 'left' |

| label | In downward sampling, mark the aggregation results with the box label of 'right' /'left '(for example, the 5-minute interval from 9:30 to 9:35 can be marked as 9:30 / 9:35) |

| loffset | Adjust the time of the box label (for example, '1s' / Second(-1) can move the aggregate label forward for 1 second) |

| limit | When filling forward or backward, the maximum value of the filling interval |

| kind | Specify that the index in the result is interval ('period ') or timestamp ('timestamp'), and the default is time series index |

| convention | When resampling an interval, the convention used to convert a low-frequency period to a high-frequency period is' start 'by default and' end 'is optional |

Down sampling

Things to consider when using resample() to sample down:

- Which side of each interval is closed

- How to mark each aggregated box at the beginning or end of the interval

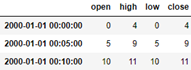

rng = pd.date_range('2000-01-01', periods=12, freq='T')

ts = pd.Series(np.arange(12), index=rng)

ts

'''

2000-01-01 00:00:00 0

2000-01-01 00:01:00 1

2000-01-01 00:02:00 2

2000-01-01 00:03:00 3

2000-01-01 00:04:00 4

2000-01-01 00:05:00 5

2000-01-01 00:06:00 6

2000-01-01 00:07:00 7

2000-01-01 00:08:00 8

2000-01-01 00:09:00 9

2000-01-01 00:10:00 10

2000-01-01 00:11:00 11

Freq: T, dtype: int32

'''

# The default is closed='left ', which divides the index interval into [00:00,00:05], [00:05,00:10),

# Then aggregate the data at such intervals

# By default, label='left ', the left side of the index interval is taken as the row label in the result

ts.resample('5min', closed='left').sum()

'''

2000-01-01 00:00:00 10

2000-01-01 00:05:00 35

2000-01-01 00:10:00 21

Freq: 5T, dtype: int32

'''

ts.resample('5min', closed='right').sum()

'''

1999-12-31 23:55:00 0

2000-01-01 00:00:00 15

2000-01-01 00:05:00 40

2000-01-01 00:10:00 11

Freq: 5T, dtype: int32

'''

ts.resample('5min', closed='right', label='right').sum()

'''

2000-01-01 00:00:00 0

2000-01-01 00:05:00 15

2000-01-01 00:10:00 40

2000-01-01 00:15:00 11

Freq: 5T, dtype: int32

'''

# Setting loffset='1s' will move the index in the result to the right for 1 second, that is, add 1 second

ts.resample('5min', closed='right',

label='right', loffset='1s').sum()

'''

2000-01-01 00:00:01 0

2000-01-01 00:05:01 15

2000-01-01 00:10:01 40

2000-01-01 00:15:01 11

Freq: 5T, dtype: int32

'''

Start peak valley end (OHLC) resampling

# ohlc() gets the first value, the last value, the maximum value, and the minimum value within the index interval

ts.resample('5min').ohlc()

Up sampling and difference

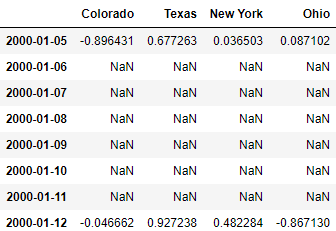

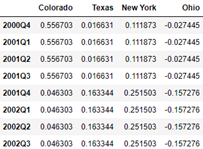

# When upsampling, aggregation is not required, and asfreq() is used for frequency conversion

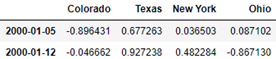

frame = pd.DataFrame(np.random.randn(2, 4),

index=pd.date_range('1/1/2000', periods=2,

freq='W-WED'),

columns=['Colorado', 'Texas', 'New York', 'Ohio'])

frame

# When asfreq() is used for frequency conversion, missing values will be introduced when converting from low frequency to high frequency

df_daily = frame.resample('D').asfreq()

df_daily

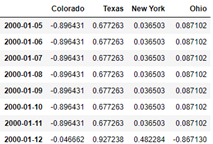

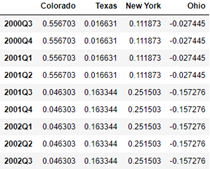

# If you do not want to introduce the missing value, you can set the filling value with fill()

frame.resample('D').ffill()

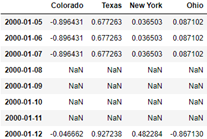

# If limit=2 is passed to fill(), only two rows of data will be filled forward

frame.resample('D').ffill(limit=2)

frame.resample('W-THU').ffill()

Resampling with Periods

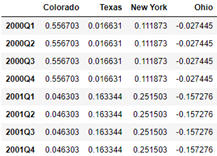

frame = pd.DataFrame(np.random.randn(24, 4),

index=pd.period_range('1-2000', '12-2001',

freq='M'),

columns=['Colorado', 'Texas', 'New York', 'Ohio'])

frame[:5]

# Downward sampling, frequency 'A-DEC', year, December as the last month at the end of the year

annual_frame = frame.resample('A-DEC').mean()

annual_frame

# Sample upward and set the fill method fill(), with the default convention='start '

# Q-DEC: quarter, December is the last month of the last quarter

annual_frame.resample('Q-DEC').ffill()

# Sample upward and set the filling method fill()

# Pass convention='end ', set the index in the result to start at the end of the quarter of the original first index year and end at the end of the quarter of the original last index year

annual_frame.resample('Q-DEC', convention='end').ffill()

In down sampling, the frequency in the original sequence must be the sub interval of the frequency in the result; Month year

When sampling upward, the frequency in the original sequence must be the parent interval of the frequency in the result; Year month

Carefully figure out the following operations and understand them through drawing

annual_frame.resample('Q-MAR').ffill()

annual_frame.resample('Q-MAR', convention='end').ffill()

annual_frame.resample('Q-APR').ffill()

annual_frame.resample('Q-APR', convention='end').ffill()

7, Move window function

Like other statistical functions, the moving window function will automatically exclude missing data

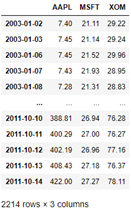

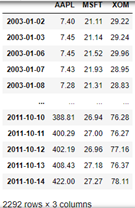

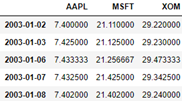

close_px_all = pd.read_csv('examples/stock_px_2.csv',

parse_dates=True, index_col=0)

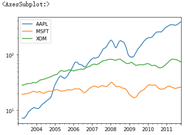

close_px = close_px_all[['AAPL', 'MSFT', 'XOM']]

close_px

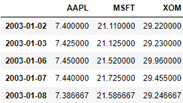

# Resampling according to working day frequency

close_px = close_px.resample('B').ffill()

close_px

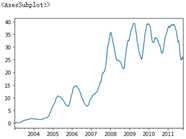

%matplotlib inline close_px.AAPL.plot() # rolling() can be called through a window (i.e. the number 250 passed in below) on Series and DataFrame # Here is the grouping according to 250 sliding windows close_px.AAPL.rolling(250).mean().plot()

# Transfer min_ If periods = 10, the standard deviation of the first 10 closed transactions will be calculated first, then the standard deviation of the first 11 transactions, and so on # Until the first 250 groups of data are calculated, the moving window is used to calculate the standard deviation appl_std250 = close_px.AAPL.rolling(250, min_periods=10).std() appl_std250[5:12] ''' 2003-01-09 NaN 2003-01-10 NaN 2003-01-13 NaN 2003-01-14 NaN 2003-01-15 0.077496 2003-01-16 0.074760 2003-01-17 0.112368 Freq: B, Name: AAPL, dtype: float64 ''' appl_std250.plot()

# expanding() will make the window expand gradually. The left side will not move and the right side will expand to the right; Find the mean value of the extended window # For example, here, 2003-01-16 is the average of the original 01-16 and 01-15 # For example, here, 2003-01-17 is the average value of the original 01-15 to 01-17 expanding_mean = appl_std250.expanding().mean() expanding_mean[5:12] ''' 2003-01-09 NaN 2003-01-10 NaN 2003-01-13 NaN 2003-01-14 NaN 2003-01-15 0.077496 2003-01-16 0.076128 2003-01-17 0.088208 Freq: B, Name: AAPL, dtype: float64 ''' # Pass log = true and take the logarithm of y close_px.rolling(60).mean().plot(logy=True)

# Pass' 20D ', fixed to 20 days of the calendar day for moving; In the previous pass, 250 days of the index column is taken as a window

close_px.rolling('20D').mean().head()

# Pass' 3D ', fixed to take the 3 days of the calendar day for moving average

# Therefore, the mean value of 2003-01-06 in the results remains unchanged because there are no data on No. 4 and No. 5

close_px.rolling('3D').mean().head()

Exponential weighting function

# Specify the attenuation factor through span=30, that is, the weights are 2 / 31, 2 / 31 * 29 / 31 aapl_px = close_px.AAPL['2006':'2007'] # Simple moving average ma60 = aapl_px.rolling(30, min_periods=20).mean() # Exponential weighted average ewma60 = aapl_px.ewm(span=30).mean() ma60.plot(style='k--', label='Simple MA') ewma60.plot(style='k-', label='EW MA') plt.legend()

Binary moving window function

Operate two time series at the same time, using the same moving window size, such as corr() or covariance

spx_px = close_px_all['SPX']

spx_rets = spx_px.pct_change()

spx_rets

'''

2003-01-02 NaN

2003-01-03 -0.000484

2003-01-06 0.022474

2003-01-07 -0.006545

2003-01-08 -0.014086

...

2011-10-10 0.034125

2011-10-11 0.000544

2011-10-12 0.009795

2011-10-13 -0.002974

2011-10-14 0.017380

Name: SPX, Length: 2214, dtype: float64

'''

returns = close_px.pct_change()

returns

# Notice here, returns AAPL has 2292 rows of data, while spx_rets has 2214 rows of data # Therefore, their row indexes are not exactly the same when calculating mobile windows # Under normal circumstances, this will not happen. It may be the author's mistake # corr() calculates the rolling correlation coefficient corr = returns.AAPL.rolling(125, min_periods=100).corr(spx_rets) corr.plot()

corr = returns.rolling(125, min_periods=100).corr(spx_rets) corr.plot()

User defined moving window function

# Using apply() on rolling() and related methods can use custom array functions in the moving window from scipy.stats import percentileofscore # What percentage of samples x is less than 0.02 score_at_2percent = lambda x: percentileofscore(x, 0.02) result = returns.AAPL.rolling(250).apply(score_at_2percent) result.plot()