Chapter 2 linear regression

2.1 simple linear regression

The ISLR2 library contains the Boston dataset, which records medv (median house value) for 506 census districts in Boston.

We will use 12 predictive variables, such as rmvar (average number of rooms per household), age (average house age), and lstat (percentage of households with low socio-economic status), to predict medv.

library(ISLR2) library(MASS)

head(Boston)

| crim | zn | indus | chas | nox | rm | age | dis | rad | tax | ptratio | black | lstat | medv | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <int> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | |

| 1 | 0.00632 | 18 | 2.31 | 0 | 0.538 | 6.575 | 65.2 | 4.0900 | 1 | 296 | 15.3 | 396.90 | 4.98 | 24.0 |

| 2 | 0.02731 | 0 | 7.07 | 0 | 0.469 | 6.421 | 78.9 | 4.9671 | 2 | 242 | 17.8 | 396.90 | 9.14 | 21.6 |

| 3 | 0.02729 | 0 | 7.07 | 0 | 0.469 | 7.185 | 61.1 | 4.9671 | 2 | 242 | 17.8 | 392.83 | 4.03 | 34.7 |

| 4 | 0.03237 | 0 | 2.18 | 0 | 0.458 | 6.998 | 45.8 | 6.0622 | 3 | 222 | 18.7 | 394.63 | 2.94 | 33.4 |

| 5 | 0.06905 | 0 | 2.18 | 0 | 0.458 | 7.147 | 54.2 | 6.0622 | 3 | 222 | 18.7 | 396.90 | 5.33 | 36.2 |

| 6 | 0.02985 | 0 | 2.18 | 0 | 0.458 | 6.430 | 58.7 | 6.0622 | 3 | 222 | 18.7 | 394.12 | 5.21 | 28.7 |

To learn more about datasets, we can type? Boston.

We will first use lm () function to fit a simple linear regression model,

medv was used as the explained variable and lstat was used as the explanatory variable.

lm.fit <- lm(medv~lstat, data = Boston)

lm.fit

Call:

lm(formula = medv ~ lstat, data = Boston)

Coefficients:

(Intercept) lstat

34.55 -0.95

summary(lm.fit)

Call:

lm(formula = medv ~ lstat, data = Boston)

Residuals:

Min 1Q Median 3Q Max

-15.168 -3.990 -1.318 2.034 24.500

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 34.55384 0.56263 61.41 <2e-16 ***

lstat -0.95005 0.03873 -24.53 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.216 on 504 degrees of freedom

Multiple R-squared: 0.5441, Adjusted R-squared: 0.5432

F-statistic: 601.6 on 1 and 504 DF, p-value: < 2.2e-16

We can use the names () function to find out what other information is stored in lm. We can extract these quantities by name,

For example, LM Fit $coefficients, which are more secure to access using extractor functions such as coef ().

names(lm.fit)

- 'coefficients'

- 'residuals'

- 'effects'

- 'rank'

- 'fitted.values'

- 'assign'

- 'qr'

- 'df.residual'

- 'xlevels'

- 'call'

- 'terms'

- 'model'

(Intercept) 34.5538408793831 lstat -0.95004935375799# correlation coefficient coef(lm.fit)

# confidence interval confint(lm.fit)

| 2.5 % | 97.5 % | |

|---|---|---|

| (Intercept) | 33.448457 | 35.6592247 |

| lstat | -1.026148 | -0.8739505 |

The predict() function can be used to generate confidence intervals and prediction intervals to predict the medv of a given lstat value.

predict(lm.fit, data.frame(lstat = c(5,10,15)), interval = 'prediction')

| fit | lwr | upr | |

|---|---|---|---|

| 1 | 29.80359 | 17.565675 | 42.04151 |

| 2 | 25.05335 | 12.827626 | 37.27907 |

| 3 | 20.30310 | 8.077742 | 32.52846 |

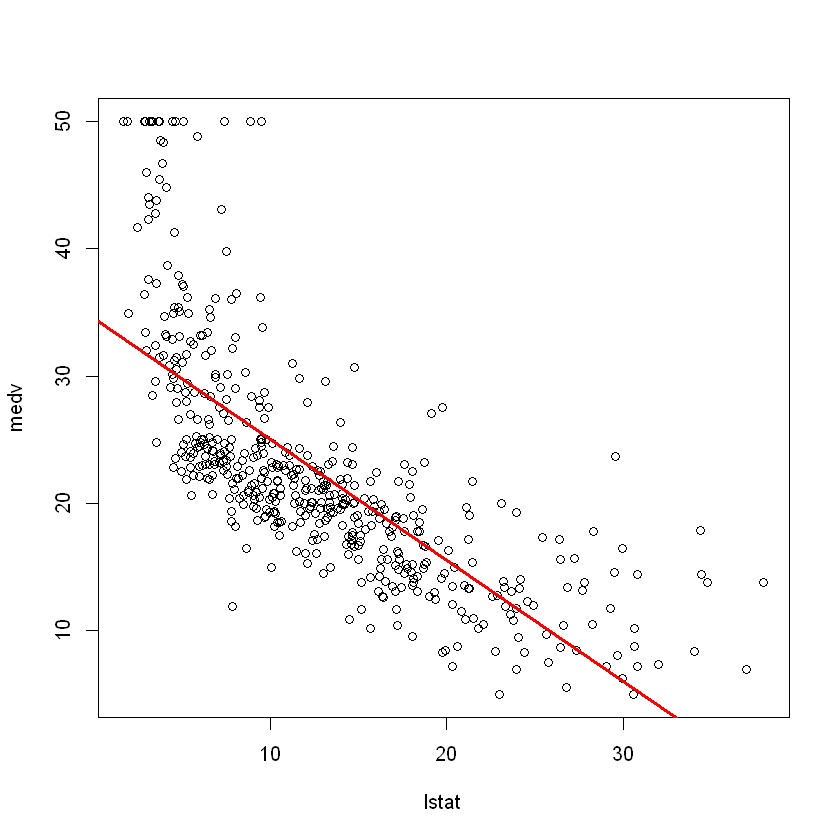

attach(Boston) plot(lstat, medv) abline(lm.fit)

The function is used to draw any straight line, not just the least squares regression line. To draw a line with intercept a and slope B, we need to type a line (a, b). Next, we'll experiment with some additional settings for lines and points. The lwd=3 command increases the width of the regression line by 3 times;

This also applies to the plot () and lines () functions. We can also use the pch option to create different symbols.

plot(lstat, medv) abline(lm.fit, lwd = 3, col='red')

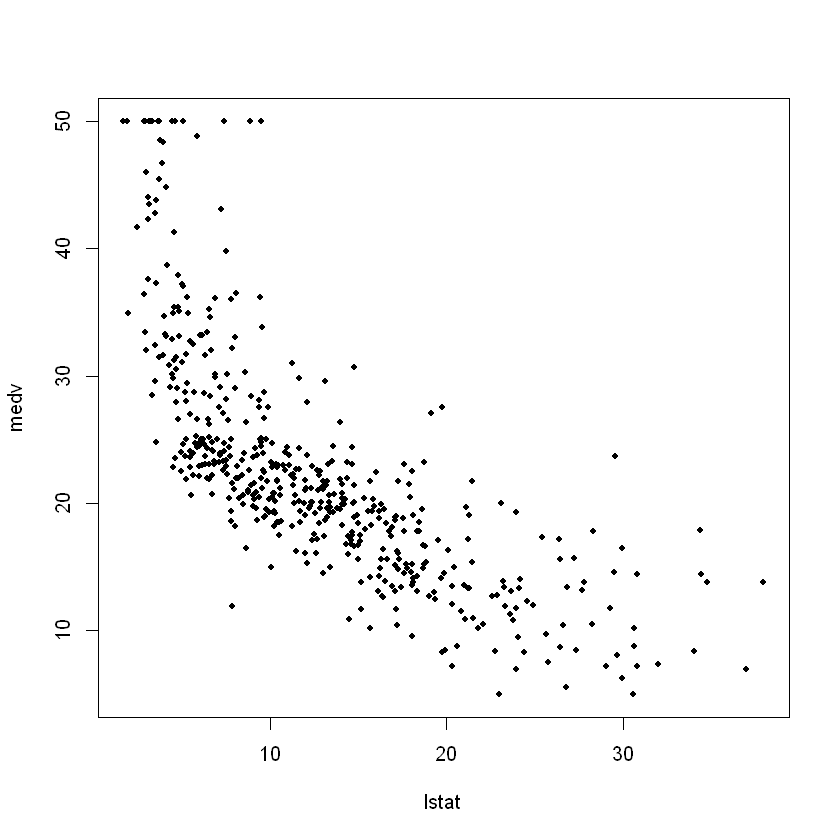

plot(lstat, medv, pch = 20)

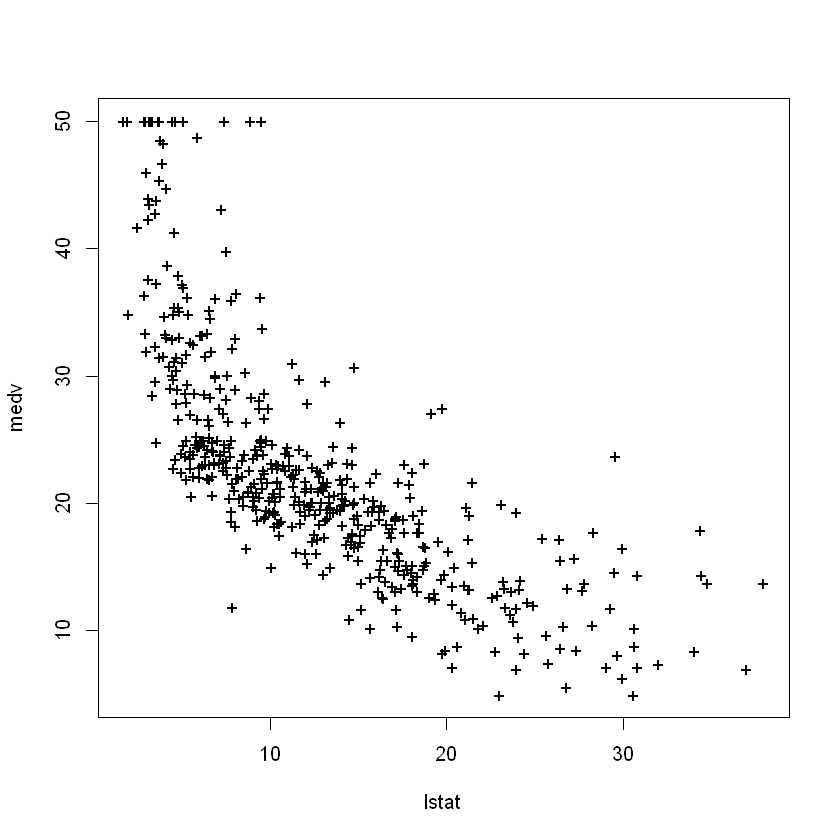

plot(lstat, medv, pch = "+")

plot(1:20, 1:20, pch = 1:20)

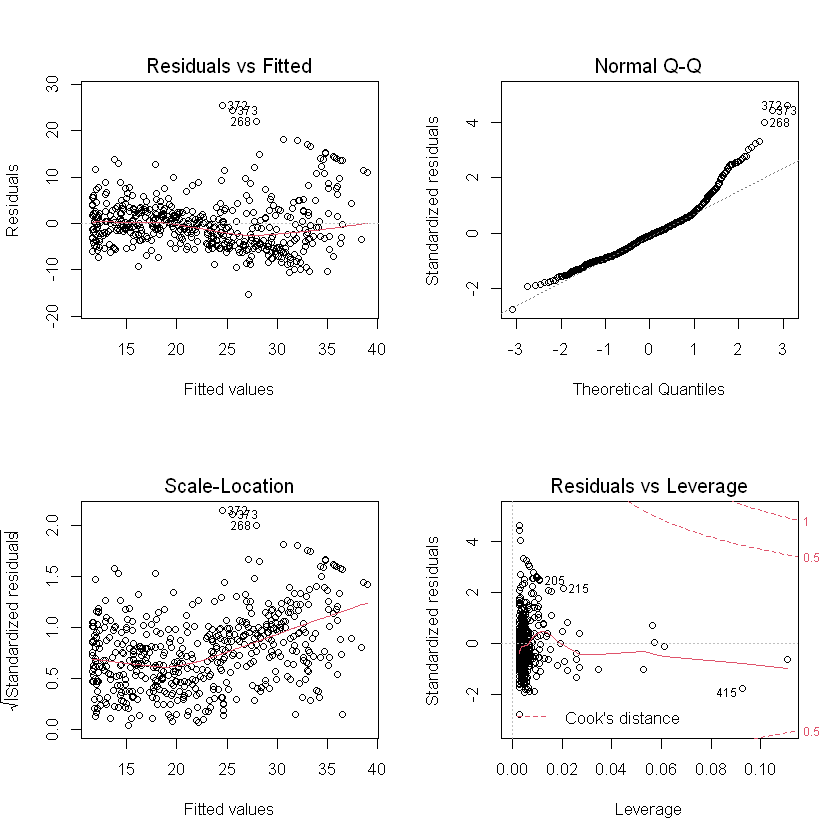

par(mfrow = c(2, 2)) plot(lm.fit)

which.max(hatvalues(lm.fit))

375: 375

which. The max() function identifies the index of the largest element in the vector. In this case, it tells us which observation has the largest leverage statistics.

2.2 multiple linear regression

In order to use the least square method to fit the multiple linear regression model, we use the lm () function again, and the summary () function now outputs the regression coefficients of all predicted values.

mfit <- lm(medv~lstat + age) summary(mfit)

Call:

lm(formula = medv ~ lstat + age)

Residuals:

Min 1Q Median 3Q Max

-15.981 -3.978 -1.283 1.968 23.158

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 33.22276 0.73085 45.458 < 2e-16 ***

lstat -1.03207 0.04819 -21.416 < 2e-16 ***

age 0.03454 0.01223 2.826 0.00491 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.173 on 503 degrees of freedom

Multiple R-squared: 0.5513, Adjusted R-squared: 0.5495

F-statistic: 309 on 2 and 503 DF, p-value: < 2.2e-16

The Boston data set contains 12 variables, so it will be troublesome to type all these variables in order to use all the predicted values for regression. Instead, we can use the following abbreviations:

lm.fit <- lm(medv ~ ., data = Boston) summary(lm.fit)

Call:

lm(formula = medv ~ ., data = Boston)

Residuals:

Min 1Q Median 3Q Max

-15.595 -2.730 -0.518 1.777 26.199

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.646e+01 5.103e+00 7.144 3.28e-12 ***

crim -1.080e-01 3.286e-02 -3.287 0.001087 **

zn 4.642e-02 1.373e-02 3.382 0.000778 ***

indus 2.056e-02 6.150e-02 0.334 0.738288

chas 2.687e+00 8.616e-01 3.118 0.001925 **

nox -1.777e+01 3.820e+00 -4.651 4.25e-06 ***

rm 3.810e+00 4.179e-01 9.116 < 2e-16 ***

age 6.922e-04 1.321e-02 0.052 0.958229

dis -1.476e+00 1.995e-01 -7.398 6.01e-13 ***

rad 3.060e-01 6.635e-02 4.613 5.07e-06 ***

tax -1.233e-02 3.760e-03 -3.280 0.001112 **

ptratio -9.527e-01 1.308e-01 -7.283 1.31e-12 ***

black 9.312e-03 2.686e-03 3.467 0.000573 ***

lstat -5.248e-01 5.072e-02 -10.347 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.745 on 492 degrees of freedom

Multiple R-squared: 0.7406, Adjusted R-squared: 0.7338

F-statistic: 108.1 on 13 and 492 DF, p-value: < 2.2e-16

summary(lm.fit)$r.sq$ R 2 {R^2} R2, (lm.fit) $sigma provides us with RSE. The Vif () function is part of the car package and can be used to calculate the variance expansion coefficient.

library(car)

Warning message: "package 'car' was built under R version 4.0.5" Loading required package: carData Warning message: "package 'carData' was built under R version 4.0.3"

crim 1.79219154743324 zn 2.29875817874944 indus 3.99159641834602 chas 1.07399532755379 nox 4.39371984757748 rm 1.93374443578326 age 3.10082551281533 dis 3.95594490637272 rad 7.48449633527445 tax 9.00855394759706 ptratio 1.79908404924889 black 1.34852107640637 lstat 2.94149107809193vif(lm.fit)

What if we want to perform regression with all variables except one? For example, in the above regression output, age has a higher p value. Therefore, we may want to run a regression that does not include this prediction. The following syntax leads to regression using all predictors except age.

mfit2 <- lm(medv ~.- age, data=Boston) summary(mfit2)

Call:

lm(formula = medv ~ . - age, data = Boston)

Residuals:

Min 1Q Median 3Q Max

-15.6054 -2.7313 -0.5188 1.7601 26.2243

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 36.436927 5.080119 7.172 2.72e-12 ***

crim -0.108006 0.032832 -3.290 0.001075 **

zn 0.046334 0.013613 3.404 0.000719 ***

indus 0.020562 0.061433 0.335 0.737989

chas 2.689026 0.859598 3.128 0.001863 **

nox -17.713540 3.679308 -4.814 1.97e-06 ***

rm 3.814394 0.408480 9.338 < 2e-16 ***

dis -1.478612 0.190611 -7.757 5.03e-14 ***

rad 0.305786 0.066089 4.627 4.75e-06 ***

tax -0.012329 0.003755 -3.283 0.001099 **

ptratio -0.952211 0.130294 -7.308 1.10e-12 ***

black 0.009321 0.002678 3.481 0.000544 ***

lstat -0.523852 0.047625 -10.999 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.74 on 493 degrees of freedom

Multiple R-squared: 0.7406, Adjusted R-squared: 0.7343

F-statistic: 117.3 on 12 and 493 DF, p-value: < 2.2e-16

2.3 interactive items

The lm () function makes it easy to include interaction terms in a linear model. Syntax lstat:black tells R to include an interaction item between lstat and black. The syntax lstat*age includes lstat, age and interactive item lstat at the same time × Age as predictor; It is the abbreviation of lstat+age+lstat:age. We can also pass the converted prediction value.

summary(lm(medv ~ lstat * age, data = Boston))

Call:

lm(formula = medv ~ lstat * age, data = Boston)

Residuals:

Min 1Q Median 3Q Max

-15.806 -4.045 -1.333 2.085 27.552

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 36.0885359 1.4698355 24.553 < 2e-16 ***

lstat -1.3921168 0.1674555 -8.313 8.78e-16 ***

age -0.0007209 0.0198792 -0.036 0.9711

lstat:age 0.0041560 0.0018518 2.244 0.0252 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.149 on 502 degrees of freedom

Multiple R-squared: 0.5557, Adjusted R-squared: 0.5531

F-statistic: 209.3 on 3 and 502 DF, p-value: < 2.2e-16

2.4 nonlinear conversion

lm () function can also be used for nonlinear transformation of explanatory variables.

For example, given an explanatory variable X, we can use I (X2) to create ${X^2} $. The function I () is required because it has special meaning in the formula object;

Our packaging allows the use of standard usage in R, that is, raising X to a power of 2. We will now return medv to lstat and lstat^2.

lm.fit2 <- lm(medv ~ lstat + I(lstat^2)) summary(lm.fit2)

Call:

lm(formula = medv ~ lstat + I(lstat^2))

Residuals:

Min 1Q Median 3Q Max

-15.2834 -3.8313 -0.5295 2.3095 25.4148

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 42.862007 0.872084 49.15 <2e-16 ***

lstat -2.332821 0.123803 -18.84 <2e-16 ***

I(lstat^2) 0.043547 0.003745 11.63 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5.524 on 503 degrees of freedom

Multiple R-squared: 0.6407, Adjusted R-squared: 0.6393

F-statistic: 448.5 on 2 and 503 DF, p-value: < 2.2e-16

# The two models are compared by analysis of variance lm.fit <- lm(medv ~ lstat) anova(lm.fit, lm.fit2)

| Res.Df | RSS | Df | Sum of Sq | F | Pr(>F) | |

|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | |

| 1 | 504 | 19472.38 | NA | NA | NA | NA |

| 2 | 503 | 15347.24 | 1 | 4125.138 | 135.1998 | 7.630116e-28 |

Here, model 1 represents a linear sub model containing only one explanatory variable lstat, while model 2 corresponds to a quadratic model with two explanatory variables lstat and lstat^2. The function is used to test the hypothesis of the two models.

The null hypothesis is that both models can fit the data well, and the selected hypothesis is that the whole model is better. Here, the statistical value of F is 135 and the value of p is almost zero. This provides very clear evidence that the model containing lstat and lstat^2 is much better than the model containing only lstat. This is not surprising because earlier we saw nonlinear evidence of the relationship between medv and lstat

par(mfrow = c(2, 2)) plot(lm.fit2)

And then we see, when l s t a t 2 lstat^2 When lstat2 item is included in the model, it performs better in the residual diagram. To create a cubic fit, we can include predictions of form I (X^3). However, for higher-order polynomials, this method may begin to become troublesome. A better approach is to use the poly () function to create polynomials in lm (). For example, the following command generates a fifth order polynomial fit:

mfit5 <- lm(medv ~ poly(lstat, 5)) summary(mfit5)

Call:

lm(formula = medv ~ poly(lstat, 5))

Residuals:

Min 1Q Median 3Q Max

-13.5433 -3.1039 -0.7052 2.0844 27.1153

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 22.5328 0.2318 97.197 < 2e-16 ***

poly(lstat, 5)1 -152.4595 5.2148 -29.236 < 2e-16 ***

poly(lstat, 5)2 64.2272 5.2148 12.316 < 2e-16 ***

poly(lstat, 5)3 -27.0511 5.2148 -5.187 3.10e-07 ***

poly(lstat, 5)4 25.4517 5.2148 4.881 1.42e-06 ***

poly(lstat, 5)5 -19.2524 5.2148 -3.692 0.000247 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5.215 on 500 degrees of freedom

Multiple R-squared: 0.6817, Adjusted R-squared: 0.6785

F-statistic: 214.2 on 5 and 500 DF, p-value: < 2.2e-16

This shows that including additional polynomial terms up to fifth order can improve model fitting! However, the further study of the data shows that the polynomial terms above the fifth order have no significant p value in the regression fitting.

# Logarithmic transformation summary(lm(medv ~ log(rm), data = Boston))

Call:

lm(formula = medv ~ log(rm), data = Boston)

Residuals:

Min 1Q Median 3Q Max

-19.487 -2.875 -0.104 2.837 39.816

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -76.488 5.028 -15.21 <2e-16 ***

log(rm) 54.055 2.739 19.73 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.915 on 504 degrees of freedom

Multiple R-squared: 0.4358, Adjusted R-squared: 0.4347

F-statistic: 389.3 on 1 and 504 DF, p-value: < 2.2e-16

2.5 qualitative explanatory variables

Now we will examine the Carseats data, which is part of the ISLR2 library. We will try to predict sales in 400 locations based on some explanatory variables.

head(Carseats)

| Sales | CompPrice | Income | Advertising | Population | Price | ShelveLoc | Age | Education | Urban | US | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <fct> | <dbl> | <dbl> | <fct> | <fct> | |

| 1 | 9.50 | 138 | 73 | 11 | 276 | 120 | Bad | 42 | 17 | Yes | Yes |

| 2 | 11.22 | 111 | 48 | 16 | 260 | 83 | Good | 65 | 10 | Yes | Yes |

| 3 | 10.06 | 113 | 35 | 10 | 269 | 80 | Medium | 59 | 12 | Yes | Yes |

| 4 | 7.40 | 117 | 100 | 4 | 466 | 97 | Medium | 55 | 14 | Yes | Yes |

| 5 | 4.15 | 141 | 64 | 3 | 340 | 128 | Bad | 38 | 13 | Yes | No |

| 6 | 10.81 | 124 | 113 | 13 | 501 | 72 | Bad | 78 | 16 | No | Yes |

Car seat data includes qualitative predictors, such as shelveloc, which is an indicator of shelf position quality, that is, each position in the store shows the space of car seats. The predictor shelleloc has three possible values: bad, medium, and good. Given a qualitative variable (such as shelveloc), R will automatically generate a virtual variable. Next, we fit a multiple regression model, including some interaction terms.

lm.fit <- lm(Sales ~ . + Income:Advertising + Price:Age,

data = Carseats)

summary(lm.fit)

Call:

lm(formula = Sales ~ . + Income:Advertising + Price:Age, data = Carseats)

Residuals:

Min 1Q Median 3Q Max

-2.9208 -0.7503 0.0177 0.6754 3.3413

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6.5755654 1.0087470 6.519 2.22e-10 ***

CompPrice 0.0929371 0.0041183 22.567 < 2e-16 ***

Income 0.0108940 0.0026044 4.183 3.57e-05 ***

Advertising 0.0702462 0.0226091 3.107 0.002030 **

Population 0.0001592 0.0003679 0.433 0.665330

Price -0.1008064 0.0074399 -13.549 < 2e-16 ***

ShelveLocGood 4.8486762 0.1528378 31.724 < 2e-16 ***

ShelveLocMedium 1.9532620 0.1257682 15.531 < 2e-16 ***

Age -0.0579466 0.0159506 -3.633 0.000318 ***

Education -0.0208525 0.0196131 -1.063 0.288361

UrbanYes 0.1401597 0.1124019 1.247 0.213171

USYes -0.1575571 0.1489234 -1.058 0.290729

Income:Advertising 0.0007510 0.0002784 2.698 0.007290 **

Price:Age 0.0001068 0.0001333 0.801 0.423812

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.011 on 386 degrees of freedom

Multiple R-squared: 0.8761, Adjusted R-squared: 0.8719

F-statistic: 210 on 13 and 386 DF, p-value: < 2.2e-16

The contrasts() function returns a dummy variable

attach(Carseats) contrasts(ShelveLoc)

| Good | Medium | |

|---|---|---|

| Bad | 0 | 0 |

| Good | 1 | 0 |

| Medium | 0 | 1 |

R creates a ShelveLocGood dummy variable. If the shelving position is good, the value of the variable is 1, otherwise it is 0. It also creates a ShelveLocMedium dummy variable. If the shelving position is medium, the variable is equal to 1, otherwise it is 0. The wrong shelving position corresponds to the zero of each of the two dummy variables. The fact that the shelf commodity coefficient in the regression output is positive shows that good shelf position is related to higher sales (relative to bad position). The positive coefficient of ShelveLocMedium is small, indicating that the sales of medium shelf position is higher than that of poor shelf position, but lower than that of good shelf position.

2.6 function writing

As we can see, R comes with many useful functions, and more functions can be obtained through the R library. However, we are usually interested in performing an operation that does not have a function that can be used directly. In this setup, we may need to write our own functions. For example, below we provide a simple function called LoadLibraries (), which is used to read ISLR2 and MASS libraries. Before we create the function, if we try to call it, R will return an error.

LoadLibraries <- function(){

library(ISLR2)

library(MASS)

print("Related libraries have been imported")

}

LoadLibraries()

[1] "Related libraries have been imported"